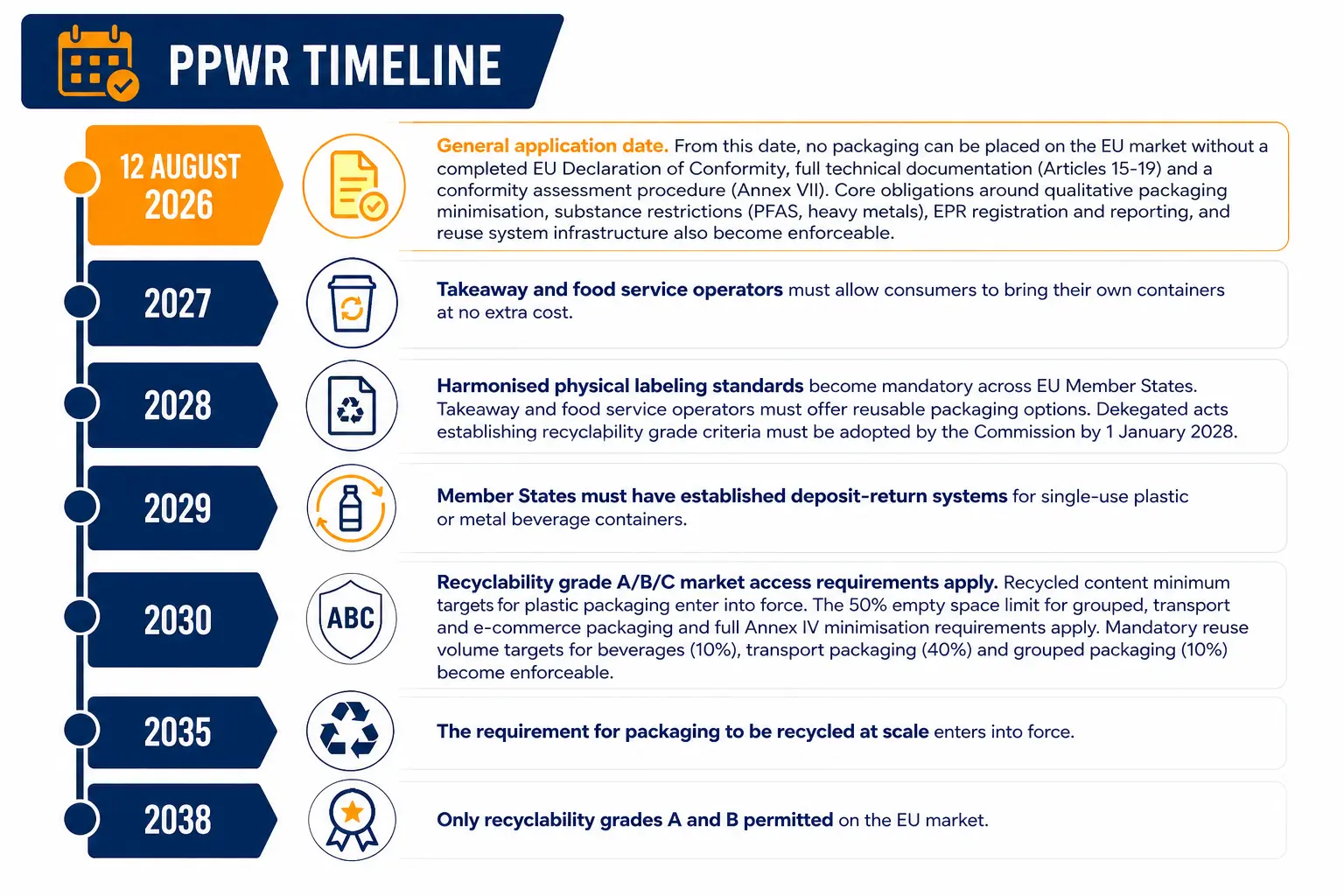

Where PPWR compliance programmes stall: seven operational failure points

The challenges that block PPWR progress are not primarily regulatory. They are operational. Each one below describes the situation as it presents in practice, not as a generic gap.

1. The inventory that does not exist

A consumer goods company with 400 SKUs across three business units begins its PPWR assessment. Six weeks in, the team realises that no consolidated packaging inventory exists. Procurement holds component data for direct-sourced packaging. The product development team has partial specs. Several legacy SKUs exist only in supplier catalogues. Until a complete component-level inventory is built, no recyclability assessment can be scoped, no substance compliance check can be run, and no DoC can be produced. This is the foundational gap, and it is more common than most organisations expect.

2. Suppliers who cannot provide what PPWR requires

Packaging suppliers are required under PPWR to provide material declarations, substance compliance confirmations and recycled content data. Many smaller suppliers lack the internal processes to generate this documentation in a structured, auditable format. When data requests go out as email attachments and responses arrive as PDFs in inconsistent formats, procurement teams face weeks of manual reconciliation before any compliance validation can begin. The problem compounds when direct suppliers source components from upstream providers who are even less prepared.

3. Recyclability status that nobody has assessed

A manufacturer with a complex packaging portfolio knows its packaging passes visual inspection but has never run a formal recyclability assessment against harmonised criteria. Several formats contain composite materials whose recyclability is unknown. Without assessment methodology aligned to the PPWR criteria, recyclability cannot be claimed or documented, and the DoC cannot be completed. Identifying which formats require redesign before August 2026 takes time that needs to be accounted for now.

4. Recycled content claims that do not hold up to audit

A supplier states that a packaging component contains 30% post-consumer recycled content. The producer includes this in its DoC. An authority requests the substantiation. The supplier cannot provide a documented calculation methodology or verifiable chain of custody evidence. The claim fails the audit. Recycled content targets under PPWR require more than a supplier statement; they require documented calculation methodology and verifiable evidence retained at the component level.

5. Compliance documentation that exists on paper but not in practice

A regulatory team produces a Declaration of Conformity. The technical file it references is distributed across three shared drives, several team email inboxes and one retired employee’s laptop. The conformity assessment procedure was completed once and never updated when packaging formulations changed. When a market surveillance authority requests the documentation set, the team needs two weeks to locate and compile it. Market surveillance requests do not come with two weeks of notice.

6. Governance that stops at the first cross-functional handoff

PPWR touches procurement, packaging design, sustainability, regulatory affairs and finance. In most organisations, no single owner has authority across all of these functions. Packaging changes require sign-off from multiple teams. Supplier switches that affect material composition trigger compliance re-assessments that nobody is assigned to run. Without a defined decision workflow and clear ownership, compliance work stalls at every cross-functional boundary.

7. EPR complexity that multiplies with every additional Member State

An organisation placing packaging on the market in Germany, France, the Netherlands, Poland and Spain faces five separate EPR registration and reporting frameworks, each with its own timelines, data formats and national authority requirements. A consolidated, validated packaging dataset is the prerequisite for feeding all of them. Companies that maintain separate national datasets, or that report from unvalidated source data, create both fee calculation errors and audit risk.